To try and create greater familiarity for those living elsewhere, we’ll periodically profile some China brands and businesses that we believe will be household names across the world soon. This month let’s look at a very interesting brand and business – Shun Feng Express Delivery (顺丰速运)- one of the leading brands in the express delivery business in China.

Background and History

Established in 1993 in Shunde city, Guangdong Province, China, Shunfeng started as a Hong-Kong to Guangdong delivery specialist. Phonetically, Shun Feng (顺风) refers to a tailwind or a favorable wind, but by changing the last character from 风 to 丰, the name also connotes abundance or prosperity, presumably attained by using the service.

Today, Shunfeng is one of the best known delivery brands in China, operating their own fleet of 50 aircraft and also providing international deliveries. Like most of the other companies in their sector, they’re a public company – listed on the Shenzhen Stock Exchange.

Financials

Despite not being the biggest in terms of deliveries, SF is the biggest in terms of revenue and operating profit amongst its competitors, which speaks to the power of the brand and its ability to command a premium with consumers (which is why we’re featuring SF rather than any of its competitors).

The first-half 2020 semi-annual report covering the period Mar-Aug 2020 shows a very healthy revenue of 71 billion RMB, which promises tremendous growth for the full year over the 112 billion RMB of 2019. Interestingly, SF leads its competitors in revenue by over 80 billion RMB, despite ranking around 6th in terms of delivery volume. That premium pricing model is clearly profitable, with the 2020 semi-annual report showing a net profit attributable to shareholders of 3.76 billion RMB.

Success Factors

SF has built a reputation with consumers by focusing on the most premium end of the market – express / overnight deliveries. The other delivery companies have tended to create more options for the consumer on slower, less expensive services, giving them a lot of volume but not the kind of pricing and margin that SF has achieved.

With the e-commerce boom in China, there is a clear opportunity to build a high volume, low margin business with a slower, cheaper delivery option. This is a sector in which all of SF’s competitors are active and SF is definitely late to this party.

Separately, there are lots of specialized delivery services springing up. Ding Dong Mai Cai – a delivery service specializing in fresh goods, for instance, is one of the recent successes that is redefining delivery with specific niches and creating new markets.

Perhaps the way forward is for SF to stay with what it’s good at – premium, express deliveries – and double down on its competitive advantages there, but whether they choose to do that or try and compete in emerging, lower margin but higher volume segments, only time will tell. Clearly though, this 28 year old company has built a high degree of consumer recognition and trust. With their already established international delivery business, their impressive fleet of 50 aircraft and their own cargo airline, it may not be long before that SF truck pulls up in your driveway.

While our focus as a consultancy is making new brands famous in China, there are many (already) famous Chinese brands that aren’t well known overseas. We will be bringing them to light in this series over time.

If you’d like your brand to be famous and successful in China reach out to us at enquiries@searchlightchina.com – we work with both local startups as well as international brands that would like to do better in this market.

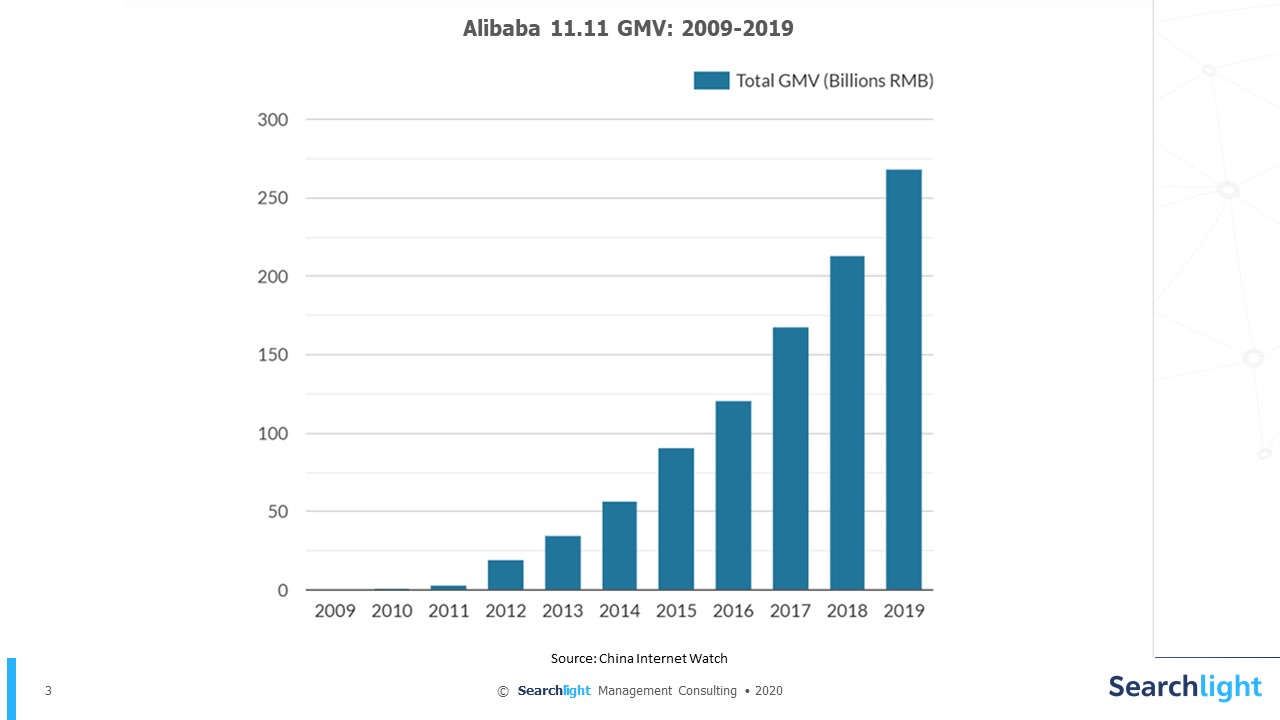

It’s interesting to look back at 2009 when this took place for the first time and note that only 27 brands took part in a one-day sale that netted about 50 million RMB in GMV. That number has grown exponentially to 268 billion RMB in 2019. More than 100 brands rang up sales of over 15 million USD (about 100 million RMB) in the first two hours of that day – each more than double the value of that first 11.11 more than a decade ago.

It’s interesting to look back at 2009 when this took place for the first time and note that only 27 brands took part in a one-day sale that netted about 50 million RMB in GMV. That number has grown exponentially to 268 billion RMB in 2019. More than 100 brands rang up sales of over 15 million USD (about 100 million RMB) in the first two hours of that day – each more than double the value of that first 11.11 more than a decade ago.