Double Eleven (11.11, or 11 Nov), a.k.a. Singles’ Day Festival is a global shopping event initiated by Alibaba and adopted by other e-commerce platforms and retailers. For those who are not familiar with it, Alibaba’s online shopping event on November 11 every year is the biggest in the world. You could say Black Friday is Amazon’s weaker, smaller version of the behemoth that is 11.11.

Alibaba dominates over 60% of online sales in China and online sales are over a quarter of retail – a very powerful position often seen as a platform for launching brands to dizzying heights of success.

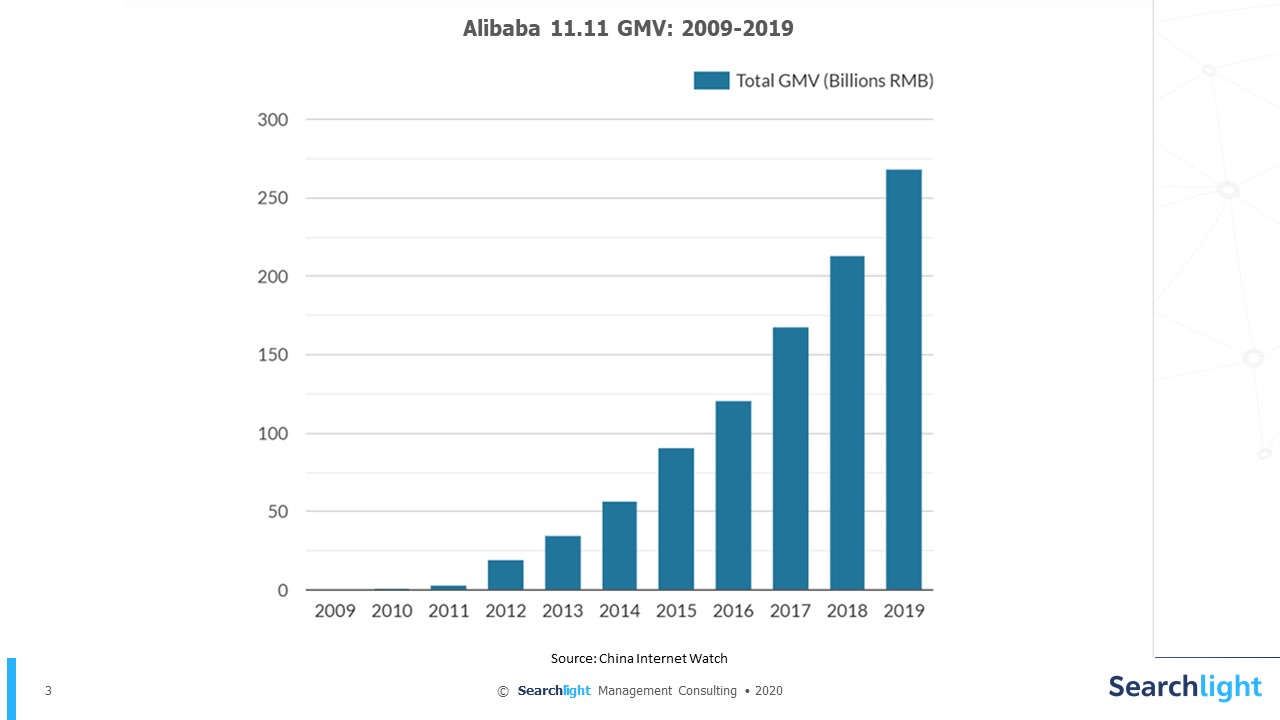

It’s interesting to look back at 2009 when this took place for the first time and note that only 27 brands took part in a one-day sale that netted about 50 million RMB in GMV. That number has grown exponentially to 268 billion RMB in 2019. More than 100 brands rang up sales of over 15 million USD (about 100 million RMB) in the first two hours of that day – each more than double the value of that first 11.11 more than a decade ago.

It’s interesting to look back at 2009 when this took place for the first time and note that only 27 brands took part in a one-day sale that netted about 50 million RMB in GMV. That number has grown exponentially to 268 billion RMB in 2019. More than 100 brands rang up sales of over 15 million USD (about 100 million RMB) in the first two hours of that day – each more than double the value of that first 11.11 more than a decade ago.

Quite apart from the overall volume and business opportunity, 11.11 is often the stage on which new brands become stars. 11 of the brands that shot to category leadership positions (within Tmall) in 2019 were completely new brands. In 2020, even before the 11th of November, 359 new brands occupied category leadership positions in the 1st phase on November 1 – ( what used to be a single day festival has already extended to a much longer period, but that’s another story) – before the festival reaches its peak spending day on the 11th.

However, it’s not all champagne and roses for brands on China’s most powerful ecommerce platform. For one thing, the rules change a little bit every year. In 2018, for instance, the shopping festival really started as early as October 20 with a presale requiring a 10% deposit, a promotion period with up to 50% value vouchers from the brand from Nov 1 to 10 and then, finally, the 24 hour period when consumers could close their orders and complete the transactions in their shopping carts on 11.11.

Brands face tremendous pressure from the channel on various fronts if they are to participate in and benefit from the tremendous momentum of this day. First, they have to meet volume, store ranking and service level criteria to participate in the festival. Then, other than platform commission, they need to support Tmall in their advertising to get access to the promotional resources from the channel. Finally, they need to guarantee that the lowest prices will be on Tmall and in addition to this, often need to provide further vouchers and discounts to drive volume. Brands also need to pay an insurance fee to cover the cost of refunds/returns after the festival.

Despite doing all this, brands don’t get to decide how their campaign gets targeted and optimized. The channel will make those decisions and the brand just gets to pay its entrance fee and see what it gets back.

Some brands can no longer afford this and are unable to pay the price to participate in the real 11.11 sale leading to some very clever tactics to try and leverage the occasion without playing Alibaba’s game.

In 2017, UNIQLO achieved RMB 100 million within the first minute on 11.11 becoming the leader of the apparel category and the 1st brand to achieve 100 million in the entire 11.11. Most interestingly they had a strategy to drive Alibaba traffic to Uniqlo’s offline retail store.

Most of the SKUs in UNIQLO shop were sold out in the first hours (probably quite deliberately) and the brand issued an apology for being out of stock online and encouraged visits to the offline retail stores offering exactly the same price as advertised on 11.11.

In subsequent years UNIQLO has tried variants on this – letting people shop online but pickup at the store as well as promoting the sale on 11.11 in-store – all of which have worked well to let it leverage the shopping frenzy of the day while avoiding a lot of the costs and loss of control on Tmall.

For a lot of smaller brands that cannot afford to spend against bigger competitors on premium in-site inventory during 11.11, they need to be clear why they’re participating and what their primary objective is in being on the platform on that day. Is it a brand building opportunity given the size of the audience? Is it a chance to reach new customers, increase trials or as a sales volume driver?

While 11.11 still remains an exciting opportunity, especially for VC funded startup brands with deep pockets, no history and nothing to lose, most mature brands are now more choiceful about how they use it. A business that is built entirely on the back of sales from this one event is harder to sustain. As part of a marketing mix that encompasses traditional brand building, social media outreach, paid & organic influencers and other elements there is often a more viable way to use Tmall and 11.11 as a means to an end, without becoming unduly dependent on a diet of promotional pricing and deep discounts to win consumers.

Jacquelyn has over 20 years experience in branding and marketing, with specific expertise in the China e-commerce ecosystem for both multinational and startup brands. She has helped several brands navigate a change from B2B to B2C business models. Reach out to her for more information and insights on branding and commerce in China.