China was the biggest box-office market in 2021 (partly aided by lockdowns in the US) and with the lifting of COVID measures, is likely to come roaring back in 2023

It’s been a long time since I’ve been to a movie hall in China. The last time I went, every alternate seat was blocked off, no food or drinks were allowed inside and people had to keep their masks on all the time. Then, once the lockdowns of 2022 started, for several months there was no question of going to the cinema at all.

China has been one of the key cinema markets in the world, but over the last few years, box-office revenue has dropped significantly (as it did everywhere else).

Two key trends that may continue to impact the future though, are the reducing share of imported movies and the increased viewing habit online instead of in movie halls.

As we noted in our 2023 China Outlook report (you can get your free copy here) Chinese consumers are expressing a desire to escape stress and also may be more open to international brands, overseas travel and the world in general in months and years to come.

That should represent an opportunity for international movie producers to get back into cinemas in China and benefit from the boost as the industry revives. However, that might mean also paying attention to the home-viewing model and working out deals with the major streaming platforms in the market.

At Searchlight, we’re optimistic about China 2023. As you re-evaluate your plans and strategies for China, reach out to us on enquiries@searchlight.com if you need advice on understanding the business opportunities and leveraging them with the right strategic choices.

China has finally emerged from zero-COVID. Once the population recovers from mass infections, we see a significant opportunity for brands and businesses to get back to growth in China in 2023 and beyond. Get our detailed report based on official economic statistics, consumer research and social media trends.

Quick – which do you think is doing better in the market? Plant-based meat or non-alcoholic beer?It may not be the one you read about more often these days...

In recent times, companies like Beyond Meat have brought plant-based meat substitutes into the public eye considerably.

However, when examining some facts and figures about meat and meat substitutes, an OECD (data.oecd.org) study shows a volume of 323 million metric tons of consumption in 2020 for all types of meat, while meat substitutes of all types accounted for 470 million kilograms in 2020 – converted to metric tons that’s only 470,000 tons. That’s a share of 0.145% – absolutely miniscule.

By contrast, non-alcoholic beer seems to be doing much better. While there isn’t a single global volume share number available as easily, total global revenue is estimated at 25 billion USD out of a total beer market of 528 billion USD – a share of 4.7%. That’s pretty significant and shows that non-alcoholic beer has made a niche for itself that somehow, plant-based meat has not.

So, based on the numbers, non-alcoholic beer is doing about 30 times better than meat-substitutes – plant-based meat being only a small part of that latter category.

The question becomes, why is it this way? And the answer, as always, lies in what consumers really want and whether or not brands are able to truly satisfy those wants.

While there doesn’t seem to be one comprehensive survey asking the same questions, surveys about why consumers choose non-alcoholic beers show a few key reasons popping up consistently. Across South-East Asian countries, reasons around “cutting down alcohol consumption” or “cutting down calories from drinking” are big reasons – suggesting that people who regularly consume alcohol choose non-alcoholic beer to control their intake. Reasons cited in European countries are similar, though usually expressed as wanting to avoid the side-effects of drinking too much alcohol (hangovers, mostly). Consistently across markets, non-alcoholic beers rate as refreshing, good-tasting, satisfying, and often even healthier than traditional soft drinks.

Surveys around why people consume plant-based meat cite two key reasons consistently – a perception that meat-substitutes / plant or soya based meat is healthier, and a perception that it is better for the planet. A US survey shows a per capita consumption of 0.3 kg of meat-substitutes a year, out of a total per capita meat consumption in excess of 98 kg. That’s a share of less than 0.03% – which suggests that even the people who cite these reasons for eating meat-substitutes aren’t eating a lot of it. Also, comparisons of the nutritional value of several different brands of plant-based burgers show that they often fail the two fundamental premises on which consumers choose them – being healthier than meat and tasting similar to meat.

Perhaps the core problem is that meat-substitutes don’t really have a clear target segment. Non-alcoholic beers aim at people who normally drink beer, but for a variety of reasons don’t want to do so. Which leaves plenty of room for something that tastes and feels like a beer but isn’t alcoholic.

Last of all, while a lot of non-alcoholic beers taste like the real thing and cost a lot less, the better tasting meat-substitutes are usually much more expensive than the real thing.

Interestingly, China is the largest market in the world for meat-substitutes, at USD 2.24 billion in 2022 (estimated) out of an estimated global total of around USD 7 billion. Also, while per capita consumption of meat-substitutes is low at 0.1 kg, it is a larger percentage of the per capita meat consumption of around 40kg, which is a signal for potential growth as meat consumption in the market grows.

All of which would seem to point to China being a better place to focus on meat-substitutes than most other markets, but doesn’t take away the challenge of segmenting consumers based on their needs and picking a segment that you can actually win in.

For deeper data and insights on how you might go about doing this in China, get in touch with us at enquiries@searchlightchina.com

The largest selling brand of BEV (battery electric vehicles, basically 100% electric) is the Chinese brand BYD (比亚迪) which has recently overtaken Tesla – a classic example of a brand that’s famous in China and actually leads its category, but isn’t known in the rest of the world.

Sales of electric vehicles continue to grow around the world, with more than 3 million units having been sold from January to May in 2022, compared to 1.7 million in the same period of 2021 (an increase of more than 80 percent). According to data from CleanTechnica, BYD produced 506,868 fully electric cars in the first half of this year, which is a market share of 15.6 percent. Meanwhile, Tesla produced only 406,869 of the cars, making up 12.6 percent of the global comparison.

BYD Auto had it’s beginnings in 2003, in Xi’an, after BYD Co. Ltd. acquired Qinchuan Machinery Works which had a license for automobile production. BYD made the world’s first production-model plug-in hybrid car, the BYD F3 compact sedan, which became China’s best-selling sedan in 2009. BYD then started expanding outside China, competing mainly on price in Africa, South America and the Middle East.

However, before venturing into automobile manufacturing, BYD Co. Ltd. was focused on rechargeable batteries – with an IPO in Hong Kong in 2002 based on it’s success in that business. The 2003 purchase was opportunistic, a chance to buy a going automobile producer from a conglomerate that wanted to get rid of it, while local government was keen to keep the factory going as a source of employment.

BYD Auto started off “reverse engineering” other cars to learn how to build them. There is a story around the founder bringing his brand-new Mercedes S-Class to his R&D center, handing over the keys to his team and instructing them to take it apart so they can study it. Over the years, BYD graduated from this to improving on what they saw and moving from internal combustion to plug-in hybrids to BEVs.

BYD Auto has some unique core strengths fueling it’s success. First, it started as a rechargeable battery company and the purchase of an auto manufacturing facility was partly to start creating a bigger market for batteries. Second, the founder is primarily an innovator and engineer who drives a culture of solving technical problems.

From being seen as a cheap, low-quality car brand, BYD has changed over the years and become one of the two leading Chinese car brands, acquired it’s own design aesthetic and from a position of strength, signed JVs with leading global automakers. The 2021 BrandZ survey of top Chinese brands shows BYD ranked 29th amongst a very broad field of ALL consumer facing brands (up from 45 the previous year) and ahead of all the other local car brands. (https://www.chinainternetwatch.com/30833/brandz-top-brands/)

China has been at the forefront of encouraging the development of hybrids and electric vehicles and BYD, SAIC and the other car manufacturers have all benefited from a faster pace of development of both consumer demand and supply-side technology in this market.

A look at the 2021 annual report reveals a revenue of 211 billion RMB at a net profit margin of 1.4%. However, almost half this revenue comes from the older BYD revenue streams of batteries and mobile handset components – with 51.09% coming from automobiles. Sales in the PRC account for 69.76% of the company’s revenue.

The original HK public company still exists but shows a small revenue of under 2 billion HK$ – clearly the China listed company is the main entity now.

With it’s strong engineering DNA, a robust brand that is now ranked well by consumers and a leading share of the global market, BYD is well-poised to build on their early success and continue to dominate the global auto market to the point where they’re famous not just in China, but around the world.

While our focus as a consultancy is making new brands famous in China, there are many (already) famous Chinese brands that aren’t well known overseas. We will be bringing them to light in this series over time.

Sometimes you miss a chance to become a household name because despite being literally in every household…you don’t have a name… does that matter?

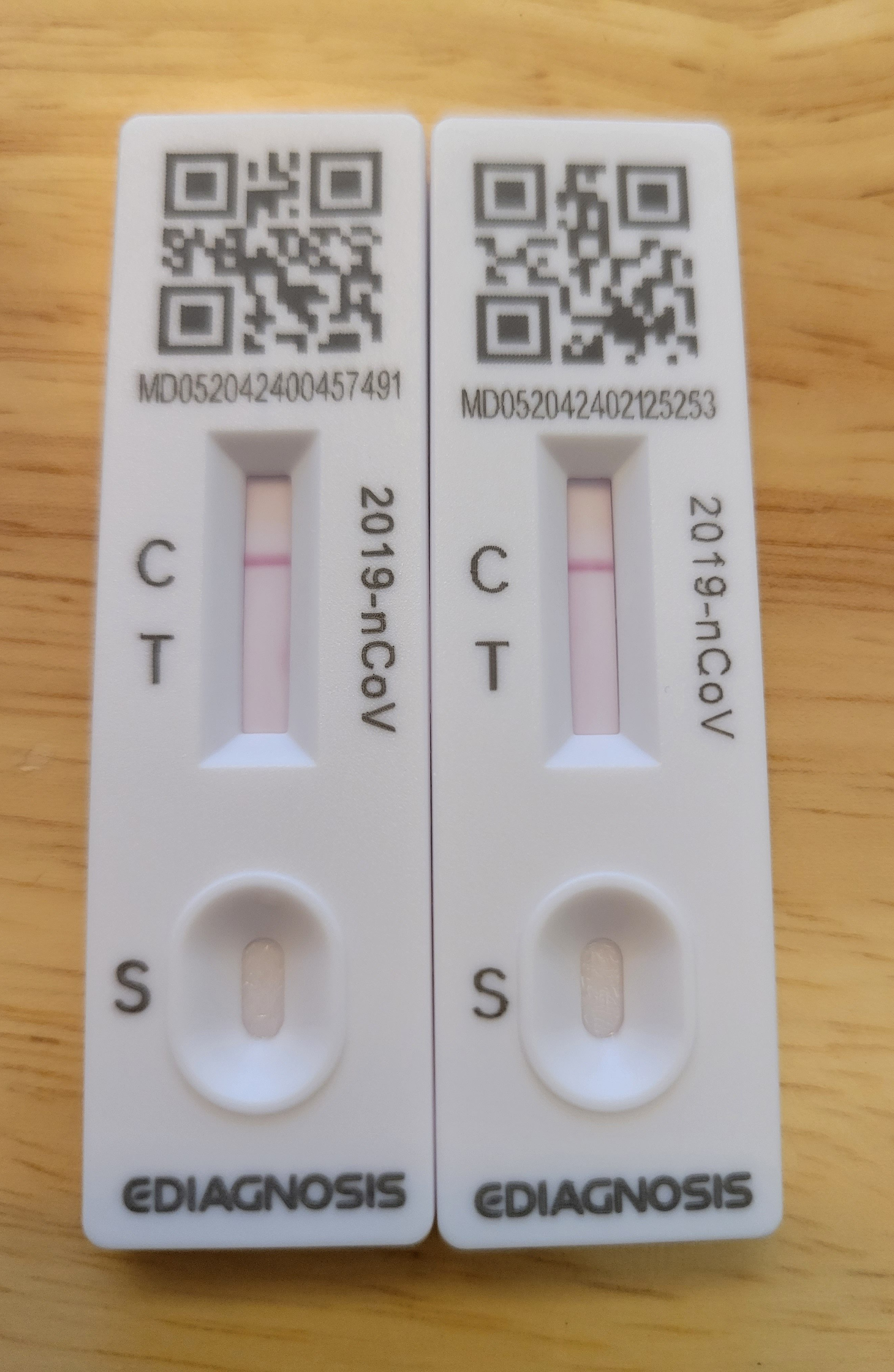

Pretty much every morning for almost 6 weeks, we started and ended our day posting our self-test result photographs within our building’s WeChat group to be collated and reported to the local authorities

Over the last few months, China went through a series of pretty strict lockdowns. Starting with Shenzhen early in the year, Shanghai from March through May and Beijing a little later, the focus on Zero-Covid has meant varying degrees of restriction on movement and importantly, a regular schedule of testing for COVID. That typically means going down for a nucleic acid test most days as well as doing two self-tests a day.

With 25 million residents in Shanghai doing 2 self-tests a day, every day for several weeks, that’s several hundred million test-kits being sold. These seem to come mostly from two companies (Zhejiang Orient Gene Biotech – http://www.orientgene.com and Wuhan Ming De Gene Biotech – mdeasydiagnostic.com).

So every day, consumers all over Shanghai and other cities (total population affected by lockdown was a staggering 140 million at its peak) are looking at one of these self-test kits twice. Close up… and they’re typically taking a photo and recording it in their neighborhood group, often also uploading it into the health-code app. In normal consumer behavior terms we’d look at that as really deep brand interactions, sharing content and so on.

Except… there’s no brand. The kits carry the name of the company, but that’s pretty meaningless since consumers aren’t familiar with it.

You could argue that it doesn’t matter – the kits are procured by the government and distributed for free at this point and having a brand wouldn’t make a difference to that.

Both companies have a global presence and ambition – Zhejiang Orient Gene apparently sells COVID self-tests in over 100 countries via government procurement and Wuhan MingDe lists various international dignitaries visiting their facilities and being given an exhibition of capabilities in this area. Clearly, being a Chinese company, their default business model is to engage with governments rather than think of engaging consumers.

What about the future though? When people buy self-test kits because they need to travel or show a negative test for their own purposes, but the population at large doesn’t need to be tested? That opportunity is going to be around for a long time – I suspect we’ll still be worrying about COVID for another 5 years or so. It is unlikely that the government will continue to be involved in procuring kits – especially outside China – for that long. Most likely there will be a set of standards for the kits, perhaps an approval process for a manufacturer to quality and then it’s up to them to distribute to consumers through the OTC channels.

On the one hand, these two companies have done remarkably well to be ready with a mass-produced self-test kit that is now reaping significant revenue rewards. However, that large-scale opportunity is unlikely to last longer than a few months and they will end up having one spectacular year in 2022 but not being able to replicate it. The bigger opportunity that they could have built on for the long-term is to build a name as a brand of self-test kits for consumers to buy whenever they need – given how COVID has evolved this is likely to be a continuing need – but they don’t have to restrict themselves to COVID or even just to self-test kits in the future. The B2C market for flu & COVID self-test kits over the next few years, especially when viewed at a global level, will be a consistent opportunity for these hitherto B2B companies to build a consistent stream of new revenue. That opportunity could have had a huge kickstart over the past two months by exploiting the twice-daily exposure to huge numbers of consumers.

The lockdowns in Shanghai and Beijing seem to be lifting and while there may be some isolated “dynamic” closures of smaller parts of these megapolises, it feels like the window of opportunity for these companies is fast closing and they’ve missed out on the chance to build a brand that can drive a new, steady revenue source for years to come.

At Searchlight Management Consulting, we can help clients navigate new business models and revenue streams that may seem unfamiliar and forbidding. Write to us at enquiries@searchlightchina.com.

Tactics is knowing what to do when there is something to do. Strategy is knowing what to do when there is nothing to do. – Chess Grandmaster Savielly Tartakower

As Shanghai enters its 8th week of city-wide lockdown, and other cities are just beginning their COVID measures, times have never been tougher for many businesses. With workers at home, factories and warehouses closed, and customers not buying, work has slowed and getting the simplest of things done can be a challenge. But with the right approach there could be a silver lining; it is possible to take advantage of the strange times we find ourselves in.

More time means time for strategy

To elaborate on Tartakower’s brilliant quote above, we tend to spend much of our working lives on the tactical; knowing what to do and getting it done before moving on to the next pressing task and leaving little time for the strategic. Over time, as the focus is on the immediate tactical tasks, the work begins to drift further and further from the original strategy.

While the lockdown has created many immediate concerns for many businesses, it may also be the opportune moment to spend the time thinking about longer-term goals, determining priorities and correcting your course.

Strike while your competitors are asleep

As Mark Ritson has shown, companies who maintain or increase their advertising spend during a recession consistently outperform their competitors once the recession is over. This is because competitors are likely to decrease their spending so the reduced clutter increases the impact (and SOV) of any advertising that continues (not in terms of sales, because the whole market is likely to be down, but in terms of consumer recall). This greater impact results in gains in market share over the short term, which are maintained in the long term and where they translate to profitability. And while China is not in a recession, there is a similar reduction in marketing budgets.

What to do while we’re still locked down

So while lockdowns, and recessions, are difficult times for many they can also be times of opportunity. To start to find those opportunities, ask yourself and your team these questions:

What are our long-term goals, and do they still apply given the current situation?

Were we on the right path to achieving those goals, or could we find a better approach given what we now know?

What are our competitors doing in response to the lockdown, and how can we capitalise on this?

Navigating the complexities of the China market is not easy at the best of times, but Searchlight is here to help you find opportunities where there seem to be none, and to help capitalise on them. Reach out to us at enquiries@searchlightchina.com.

Volunteers sorting delivery packages at the entrance of a residential compound

We’re now on day 36 of lockdowns in Shanghai (longer in Pudong) and it’s been very educational watching what consumers do, what they buy, which businesses manage to create opportunities for themselves and so on.Here are some key lessons we learned.

1. The importance of diversified supply chain

Shanghai is, after all, just one city. Even if it represents 25 or 50% of your business, there is still a market in other cities for most businesses that they can continue to service, possibly try to grow to compensate for the loss of revenue in Shanghai.

There are many companies who are unable to to do this for one simple reason – all their supply chain is in Shanghai and it’s been locked down with everything else.

While they’re trying hard to find alternative sources, it’s obviously very difficult to accomplish at short notice and while working from home.

2.The importance of diversified markets

By the same token, businesses that weren’t completely dependent on Shanghai have managed to keep their revenue chugging along – even if it’s not as healthy as before. This assumes, of course, that they weren’t entirely dependent on Shanghai for supply. Of course, Shanghai is a big market and there will be a revenue hit for a couple of months but that is less damaging than if it was your only market, which is the case for a lot of the smaller retail businesses that haven’t yet looked beyond one city.

3. Voluntary group-buys, a new (old) channel for brands to reach consumers directly:

As a preface to this point, bear in mind that big-city dwellers in China are used to a level of delivery convenience unparalleled elsewhere in the world. It was feasible to order a single drink (bubble-tea and such) because delivery costs were so low and it was possible for a delivery courier to show up right at your doorstep.

Obviously during lockdowns, couriers aren’t allowed beyond the main gate of a compound, most restaurants are closed anyway, most couriers are in the lockdown as well and no volunteer in a compound is going to appreciate making deliveries of small individual items – so that entire ecosystem crashed completely.

However, what took over very swiftly is various forms of group buys orchestrated via informal groups on WeChat (mostly). Residents of a building or compound coming together to meet a minimum order requirement for all kinds of things – from essentials like vegetables and dry goods to coffee, indulgences like KFC, Shake Shack and wine. After the initial few weeks of short supply, almost everything is now available through these channels and companies that have found ways to quickly build delivery capability and social media groups of their consumers have rescued at least some revenue through these means.

What’s particularly interesting about this new development is the brand-new, direct channel to groups of consumers who have self-selected themselves as being interested in a brand or category. Premium coffee drinkers ordering Nespresso pods, for example – under normal circumstances it would have been really difficult for a brand to find them – during the lockdown it’s become really easy because people are voluntarily registering to set up group buying, finding participants, collecting the money and placing the orders. Why should this stop when the lockdown ends? It’s a golden opportunity for brands to bypass normal distribution channels and sell directly to these consumers.

Incidentally, purchases during the lockdown weren’t just food / consumables / classic FMCG. Two appliances that have done really well (anecdotally, we don’t yet have hard data for this) are refrigerators – especially the smaller ones used as extra cold storage – and air-fryers. Given the number of people who would normally never cook for themselves who are now forced to do so, there are probably other kitchen appliances as well that have had some new opportunities come up during lockdown. Of course, if they weren’t adequately stocked in Shanghai before the lockdown started, that opportunity has passed them by.

Of course, lockdowns are (hopefully) not frequent, recurring events – for the most part it makes sense for businesses to optimize for business as usual, but these circumstances at least raise the question of having a plan B in place. Also, problems or crises often bring opportunities of their own, some of which can become long-term and very valuable for businesses that think differently and move quickly.

If your business in China is facing challenges that you’d like help to navigate, reach out to us at enquiries@searchlightchina.com

As Shanghai enters the 12th day of what was originally billed as a 4 day lockdown, the impact on businesses is very visible. We have clients who are affected and looking at their struggles and financial reforecasts for the year gives us a sense of the pain that many industries will face in China this year.

Nowhere is this more marked than retail and hospitality – businesses that depend entirely on people being able to move about freely. For this piece, we’ll focus on the hospitality business, the impact of the latest round of lockdown in Shanghai and some thoughts on what to do going forward.

We went back and looked at some statistics from 2020 when the pandemic first hit and there was a round of closures / voluntary quarantine and so forth. Bear in mind that then, it was countrywide measures whereas now we’re looking at far stricter measures but only for key cities and affected areas.

What stood out was a sharp drop in room occupancy (71.4% in Beijing and 63.9% in Shanghai) that led to corresponding drops in REVPAR (75% and 69% respectively). Revenue for all star hotels in China in 2020 dropped from 671 billion RMB in 2019 to 461 billion, the first time since 2014 that the industry shrank. Back in 2020, 73% of all hotels in China closed for an average of 27 days during January / February 2020 – which was the peak CNY travel season.

All of which goes to show that lockdowns in 2022 will have similar, deep, painful impact on the hotel industry – even if it’s not nationwide this time around. Since 2020, domestic travel within China has slowed and international travel to China has slowed even more, with only citizens and work / residence visa holders allowed back, so the industry still hasn’t recovered from the blows of 2 years ago.

One interesting dynamic that came up as China worked out a quarantine policy around April 2020 was the creation of the “quarantine hotel” business model. Hotels from almost every star category feature in the list of approved quarantine hotels where incoming travelers have to stay for 14 days, paying for their own rooms and meals. By and large, room rates are similar to normal rates, meals are fairly basic and not provided by the hotel kitchen, and there is no housekeeping for the duration of your stay – so it seems like a good way for a hotel to keep revenue going during this time. On the downside, however, there are some very tangible cost issues around putting in more manpower to ensure contactless delivery of meals, disinfection, keeping track of each patient’s quarantine history and so forth. Staff are also reluctant to work in a quarantine hotel since there is some additional risk of being infected. Most important is the risk that being branded a “quarantine” hotel may adversely affect the brand in years to come, with people reluctant to visit it just after these measures end.

What can you do if you’re running a hotel and need to find ways to survive the next 12-24 months as China continues to pursue strict lockdowns and other restrictions to achieve zero-COVID? Clearly, travel is a fickle source of income since you could open up this week and be shut down again next month. How can you drive revenue up and costs down without diluting or losing your brand for the long term?

There is no one-size-fits-all type of answer here but the core of it lies in redefining a local market that you can serve which is not dependent on travel, is available in any time but a total lockdown of the city and is either light on resources or delivers consistent long-term revenue. Depending on your hotel positioning, location and the typical consumer profiles you serve there are a few different ways to approach this which we can help you think about.

At Searchlight, we work with domain-experts in various fields as and when needed. We have access to experts from the hospitality industry who work with us to help clients address their short-term business pressures without losing sight of their long-term brand health. Get in touch at enquiries@searchlightchina.com to find out more.

MNCs often find it hard to manage their China business. Local teams insist that it’s different and needs a unique approach. Regional and global teams are worried about departing from a brand framework and business strategy that’s proven successful everywhere else in the world. How can you frame this interaction positively and help the business move forward?

We work with a mix of MNC and local clients. The local clients are typically what we’d call “mature startups” – they’ve proven the viability of a business model, have a decent amount of funding and are in the process of scaling up.

With the MNC businesses, we’re usually dealing with something that’s been around for at least a few years, done very well at one point and then declined precipitously thereafter. We often find that the local marketing / business team in China has a very different view of the market and the challenges than their counterparts from global or regional management. Given that the business has not progressed in recent years, the China team is required to do a lot more in terms of aligning their global colleagues before getting approval for any of their strategies or support for new product development / special treatment for China.

It’s hard to generalize and say why the global-local communications divide is so much more extreme for China than for other markets but here are a couple of factors:

The marketing ecosystem in China has fundamentally different dynamics than the rest of the world – not just different players but different roles, different routes to market and different power structures to anywhere else

Consumers in China are fundamentally different to those elsewhere and those differences are starting to increase as time goes by. The specifics of that may change from category to category but as a broad theme, people here have a different relationship with (global) brands and the purchase decision-making process is different than elsewhere

Let’s try and illustrate those two points with a few things we’ve observed or analyzed over recent years.

Ecommerce and digital environment:

ECommerce in China is far more dominant than anywhere else in the world (40%+ of retail sales) and unlike anywhere else, dominated by 3rd party platforms (over 80%). This means branded sites and control over your own brand / data in this space are far lower in China. It also means you can’t really optimize and attribute the funnel since you don’t have access to funnel data

Ease of launching a new product without a brand

Every year there is a rash of new products that launch on TMall and rapidly achieve a sales volume of RMB 500 million. Many of these then disappear in subsequent years. IF you talked to the people running these businesses they would all tell you that they don’t need any investment in branding – consumers already love their brand.

That’s not entirely true. The way ecommerce works in China it is very easy for consumers to search and discover new, unknown brands. Often, the platform or even government regulations for selling in certain categories remove all or most of the risk in buying an unknown brand and there are large numbers of consumer reviews to look at when making a purchase decision. If a new brand is able to get some initial traction, it can very quickly grow a big business, but without a real brand and with only functional benefits, it is only a question of time before someone else comes along and manages to be slightly cheaper / faster / better for long enough to take their place. However, that endless churn also creates tremendous pressure on global brands to establish a long term advantage that can outlast the relentless pressure of copycats. One other thing to note is that a lot of these new brands are funded by VCs and there is an endless flow of capital for anyone with a convincing story on how they will build a 500 million RMB business online.

Growing “patriotism” amongst Chinese consumers

While this is obviously a very broad generalization, younger Chinese consumers are showing a strong preference for local brands over global ones. This is not driven only by patriotism but also by the sheer abundance of local choices and a sense that in many categories, there are local nuances to consumer needs that “Western” brands cannot understand. A lot of that ties back into the messages of confidence in their destiny as a world leading economy and self-reliance as a nation that, as the COVID story unfolded, has set China apart from the rest of the world.

Following trends from Japan / Korea rather than the West

Particularly in beauty / cosmetics/ fashion related categories, Chinese consumers are now more likely to be influenced by trends from Japan and Korea than from anywhere else. We’ve seen this in the color contact lens category, for instance, where Korean and Japanese brands created a trend for treating contact lenses as fashion accessories rather than serious vison-correction/eye-care products. That was further enabled by the perception that lenses in China are a government regulated category and therefore even an unknown brand is risk-free (not entirely true). Add to this the tendency for following KOLs/网红 and suddenly you have an inrush of new consumers into this category with none of the behaviors that traditional eye-care consumers exhibit.

What that means for MNCs

While those are generic trends, in the context of each product category it is important to understand and interpret them, then explain them to everyone involved in a global brand and its fortunes in China. Doing so can help avoid painful experiences, failed experiments and situations where the local team and global team are unable to agree on a strategy.

In recent times we’ve worked on two such clients. In the case of one, we resolved a 3 year strategy deadlock by diagnosing and explaining market dynamics in a way that explained all of the facts, data and paradoxes that everyone had observed. That client is now moving ahead with an aligned strategy for China that is different from everywhere else. In the case of another, we recommended and are now helping to implement a Direct-To-Consumer approach for a company that’s always sold B2B2C in the past. In both cases, we were able to help explain the situation in terms which made sense to both global and local marketing teams, drive alignment around a strategy and the resources / input required from each and eventually move them forward.

Searchlight has an experienced team of marketers and strategists with both China and international experience, which gives us a perspective on the market that often serves as a bridge between local and international teams within a global company. Reach out to us at enquiries@searchlightchina.com if you think we can help you with interpreting your China business challenges.

As we look back on the client projects we worked on through 2021, one thing that stands out as a common theme across many of them is that the client already had more than enough data or research or information of various sorts to make good strategic decisions. Yet, somehow, they were usually in one of two modes – either looking for even more data and research to justify decisions or making decisions without considering any of the information they already had at hand.

In this post I’ll try and lay out why this happens and how to avoid it (apart from the obvious solution of hiring us to solve the problem, of course!)

First, some quick examples from the clients we worked on:

An online subscription platform where everyone in marketing was obsessed with growing the user base until we figured out that their main issue was the hemorrhaging of heavy users every year

A retail client with almost 30 people in the marketing department, an annual research budget well in excess of 2 million RMB and tons of research that hadn’t got a clear brand architecture in place and did every campaign starting from first principles instead of building on what they knew

A retail F&B chain intent on building more outlets instead of first understanding how to make their existing outlets profitable by getting more of their members to visit more often

There were others, of course, but I was taught long ago that 3 bullet points is all you need so I’ll stop there.

Why does this happen? To my mind, there are three fundamental reasons – sometimes driven by diametrically opposite dynamics that work in organizations at different stages of development.

Lack of understanding of what a differentiated strategy should look like

Many clients we meet don’t really understand the power of a clear strategy. They think doing what their competitors do, slightly cheaper, faster or better, will do the trick. They’re endlessly tactical in approach, always rushing to produce one more “seasonal” or “topical” campaign rather than setting up a clear long-term strategy built around a clear brand architecture

2. Disconnect between the data and the decision-makers

This happens usually because the person who has access to the data doesn’t have to make decisions and the person who’s making decisions doesn’t have access to the data.

I’ve seen it happen in a large organization where the research director thought her job was to manage the research budget and timelines for delivering the research projects marketing commissioned. She never thought about things in the context of what decisions needed to be made, what sorts of information were required, what already existed and therefore what minimum additional information needed to be generated. The head of marketing, on the other hand, never thought in that way either, so the briefs to the research team were not based in information requirements for strategic decision-making.

I’ve also seen this happen in startups where the CEO doesn’t understand marketing / consumer data, someone else is managing the consumer / transaction data but doesn’t use it to create reports or headlines for the CEO to act on.

Both of those situations lead to lack of a clear research / information management framework and break the link between strategic decision-making and the data that should guide it.

3. Lack of ownership of an overall business outcome

This is slightly linked to the previous point but a bit different, tending to happen more in larger teams where a silo mentality creeps in. The core problem is that people think they’re responsible only for one specific thing rather than understanding their role in driving an overall business outcome.

For one client, the head of marketing kept telling the entire marketing team that their job was driving traffic to the store – what happened after they got there was not their problem. They didn’t spend enough time thinking about what consumers did in the store, what they did after they bought the product and experienced it, how they then talked about it to other consumers – all essential parts of the purchase-decision-making chain and therefore of marketing strategy. Brand managers thought their role was to get briefs out the door on time so the agency could come back with campaigns – not collate everything the organization knew about the business to identify what they really needed to do to drive it forward.

At another, each “brand manager” focused on their role of driving either annual subscriptions or one-off orders without understanding that often the same consumer was behind both kinds of transactions and that there was considerable overlap between what they were all trying to do. The “consumer service hotline” people thought their job was offering compensation for damaged product rather than understanding how disappointed the consumer was and finding ways to address that disappointment with the brand. Small wonder that the brand lost large proportions of its heavy users when their subscriptions ended.

How do you avoid these situations?

Well, for starters, it’s really important to understand how information / data / research feed a good, differentiated business and marketing strategy, and what that strategy should look like. This means, right at the start and perhaps every 2-3 years, doing a thorough business and marketing review, ensuring there is a well thought-out strategy in place based on consumer, market and business knowledge.

Then, it’s important to preserve the link between information and decision-makers so that there is constant input into the ongoing progress of the business against that strategy. This means a proper MIS system so that on a regular basis, key business information is reviewed by the people who make decisions from it. A marketing head who does not know revenue and brand health data or a CEO who doesn’t know last week’s numbers can’t make good decisions about the business.

Last, it’s important that everyone in the organization sees their role in driving the holistic goal that defines success for the business. When people define their role very narrowly they are likely to miss the wood for the trees.

You’ll notice that my headline had the word “insight” in it and I’ve very cleverly avoided getting into it later on. I’m not going to get into it now either, except to say insights are what you build strategic choices on. Sometimes that means taking a leap from the data you have, sometimes it means unearthing data that other people don’t have – either way it gives you an “aha” moment on a way to build your business that isn’t entirely obvious until you see it.

At Searchlight we work with our clients to help them make better decisions about business and marketing strategy. A big part of this is creating better processes and decision-making frameworks that align different internal specialists and all internal and external information around a clear organizational objective and strategy. Reach out to us at enquiries@searchlightchina.com for more.