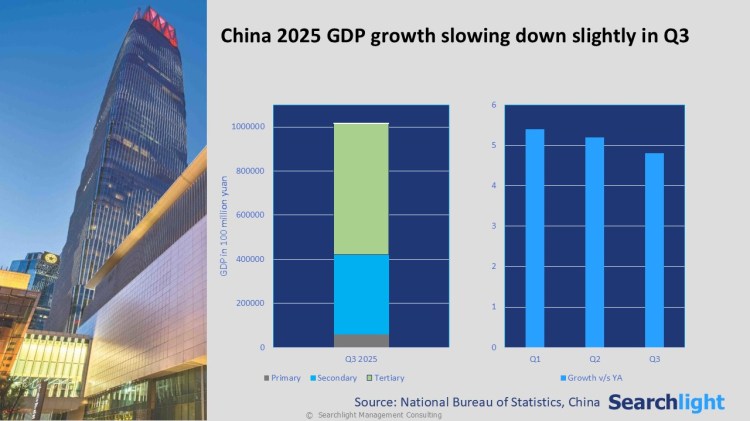

The latest economic data from China has some mixed signals. GDP is growing, although that growth rate has slowed a little bit from Q1 to Q3 of this year. Retail spending is also growing relative to 2024 but again, the growth rate is dropping as the months go by and retail spending growth drops below the GDP growth rate numbers. What might be driving this lack of consumer confidence?

The National Bureau of Statistics has released Q3 data for China and the GDP growth numbers are still positive. However, as we go from Q1 to Q3 there is a distinct slowing of the growth rate, with Q3 dropping below 5%.

The key for most businesses operating in China is, of course, consumer spending rather than GDP. Whenever those numbers exceed GDP growth, we see plenty of confidence in the economy from both businesses and consumers. However, if we look at the 2025 data, while there are a few months when consumer spending grew robustly (compared to 2024) and ahead of GDP growth, it starts to slow down as the months go by.

Even anecdotally, living in China, we notice trepidation on the part of consumers, reflected in business activities. Cab drivers often tell us their business has dropped off over the past few months, and we’re also seeing quick turnovers (closedowns and new startups) in retail service businesses around us (restaurants, spas and the like).

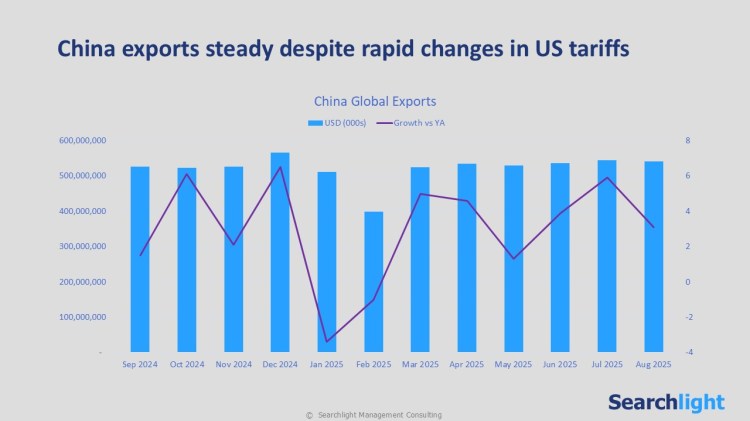

What might be driving this lack of consumer confidence? While the on-again, off-again tariff wars have the potential to affect trade, China doesn’t seem to be negatively impacted thus far. If the tariffs move from threats to actual long-term policy, there may be some effect on trade but so far there isn’t much to see here.

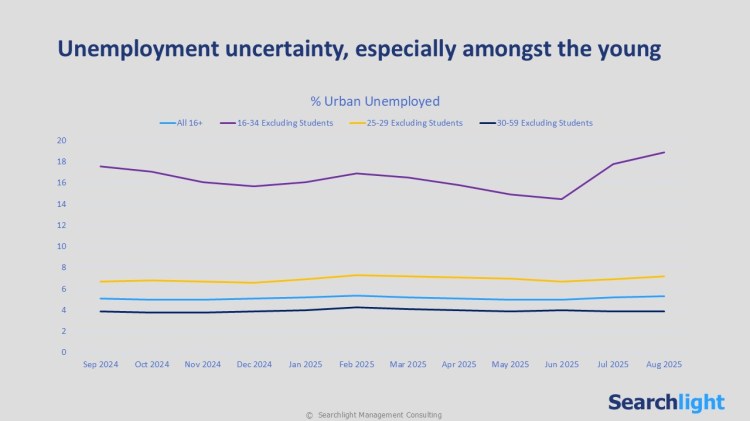

Two more likely factors might be the uncertainty of employment and the turbulence in the real-estate market caused by policy corrections in 2021 that eventually led to the collapse of Evergrande (China’s 2nd largest property developer) and similar existential crises for other players in the market.

Macroeconomic unemployment data can sometimes understate the uncertainty around employment. Looking at these figures, especially after removing students from the equation, shows that young people in particular have something quite concrete to worry about. While most young adults in China today have the safety net of inheritances from 3 families to fall back on (their parents as well as 2 sets of grandparents each), a lot of that wealth is tied up in real estate, which as we’ll see next, is also challenged.

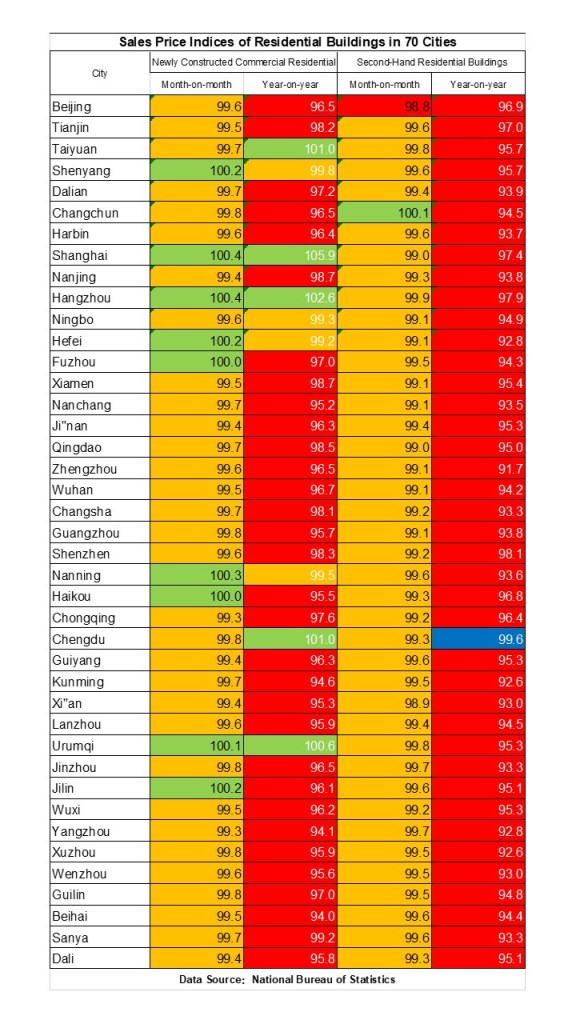

That’s a long table with lots of very small numbers on it but briefly, each number is an index. We have indices for both new buildings as well as secondhand residential sales and they’re indexed against a year ago as well as month to month. Any indices of 100 or more are in green. 99 to 100 are in orange and anything below 99 is red.

Just a glance at the table will show you a lot of red – which means for the most part, real estate values across cities are dropping an entire percentage point or more. Juxtapose that against the steady rise of real estate prices over a 30 year period and the consistent drop shows a significant trend reversal. We’ve shown 40 cities in this table, the National Bureau of Statistics has data for 70 – the trend remains the same.

So, to sum up, the economy is still growing – though there are some signs of deceleration in recent months. Consumer spending has decelerated more acutely and it seems consumers are uncertain of the future, which holds retail spending back even when the economy is growing relatively fast. Unemployment and dropping real estate prices appear to be two elements that feed that uncertainty. Unemployment is particularly noticeable amongst youth, which may explain the disproportionate effect on retail spending.

Interestingly, however, online retail spending is growing – which is a topic we’ll cover in our next post. For the moment, the key thing to bear in mind is that retail spending and GDP are still growing – businesses should continue to be cautiously optimistic, choiceful in their focus markets and strategies but continue to invest in growth opportunities.

At Searchlight Consulting, we help clients identify markets, consumer segments and brand propositions that can unlock long-term growth. Get in touch on enquiries@searchlightchina.com if you’d like to talk to us about your China growth plans.

When I first started to study economics, one of the concepts that caught my imagination was “perfect competition”.

While there are many detailed explanations of what this is, perfect competition is essentially a market with the following characteristics:

Many Buyers and Sellers: The market is made up of a huge number of independently acting firms and consumers. Each one is so small relative to the entire market that their individual decisions have zero impact on the overall market price.

Identical Products (Homogeneity): Every firm sells a product that is exactly the same as every other firm’s product. There are no brands, no quality differences, and no customer preferences for one seller over another.

Perfect Information: All buyers and sellers have complete and immediate knowledge about everything relevant to the market: prices, product quality, and available technology. No one is ever at an informational disadvantage.

Free Entry and Exit: It is very easy for a new firm to enter the market if it sees profits being made, and it is just as easy for an existing firm to leave if it’s losing money. There are no significant legal, financial, or technological barriers.

Chinese E-Commerce: The “Near-Perfect” Competition Analogy

While working on brands in China, I’ve often been blown away by the sheer number of competitors in a category, which led me to map the features of perfect competition onto the Chinese e-commerce ecosystem:

Perfect Competition Feature

Manifestation in Chinese E-Commerce

1. Many Buyers & Sellers

Extremely High. Platforms host millions of sellers, and serve hundreds of millions of buyers. The barrier to becoming a seller is incredibly low. No single small-to-medium seller has any meaningful market power.

2. Identical Products

Pseudo-Homogeneity. This is the key nuance. While products are not physically identical (like wheat), the ecosystem creates extreme substitutability. A search for “white t-shirt” or “phone charger” yields thousands of visually identical listings from different sellers. The perception of homogeneity is high.

3. Perfect Information

Asymptotically Close. Consumers have immediate access to price comparisons, detailed product images, 360-degree videos, and, most importantly, a massive volume of user reviews and ratings. Live streaming adds a layer of real-time, demonstrative information. While no one can process it all, the information is available and heavily relied upon.

4. Free Entry & Exit

Remarkably Free. Setting up a store on Taobao, Douyin, or Xiaohongshu is a process of days, not months, with minimal upfront cost. This leads to a constant churn of new entrants and failures, just as the theory predicts.

Because of these conditions, the Chinese e-commerce market exhibits core behaviors of perfect competition although, obviously, it isn’t exactly the same thing.

Extreme Price Pressure: Sellers are often forced to compete on razor-thin margins. Consumers are highly price-sensitive and will abandon a cart over a few RMB.

The “Invisible Hand” of the marketplace: The market price isn’t set by a committee but by the aggregate actions of millions, reflected in search rankings and promotional deals. Sellers are largely “price takers” relative to the platform’s prevailing price for a given product category.

The “Normal Profit” Trap: It is notoriously difficult to make sustained, high profits selling undifferentiated goods on these platforms. The moment a product gains traction, it is immediately copied and undercut by countless other sellers, quickly eroding any temporary advantage—exactly as the theory of free entry predicts.

Marketing in the Crucible of “Near-Perfect” Competition

If the market is so efficient and competitive that it grinds profits to zero, how does any brand survive?

The Two-Phase Game in China’s “Near-Perfect” Competition

Chinese e-commerce platforms like Taobao, Douyin, and Pinduoduo create a market that behaves with the ferocious efficiency of “near-perfect competition.” This environment, characterized by millions of sellers, extreme product substitutability, and perfect price information, grinds down margins and makes long-term profit seemingly impossible.

The logical conclusion was that marketing must be used to build a brand—an emotional moat—to escape this commoditization trap.

However, this misses a critical, on-the-ground reality: in China, you often must first win within the system of perfect competition before you can build a fortress to escape it. The successful playbook is not just “build a brand,” but a deliberate two-phase strategy:

Phase 1: Hack the Algorithm to Achieve Volume (The “Business” Phase)

Before a brand can have a soul, it must have a pulse. This initial phase is about survival and traction by leveraging the very rules of the hyper-competitive platform.

Focus on a Single, Razor-Sharp Attribute: Instead of a complex brand story, you focus on one undeniable, searchable value proposition. This is the antidote to homogeneity.

Examples: “The phone charger with the fastest charging time,” “The wool coat with the highest wool percentage,” “The toddler sippy cup that is 100% leak-proof.”

Master Algorithmic Marketing: This is a science. You use data from tools like Alimama (Taobao’s advertising platform) to identify high-volume, low-competition keywords. You optimize your listings (title, images, descriptions) for maximum Click-Through Rate (CTR) and conversion. The goal is to win the “invisible hand” of the algorithm, earning you precious organic visibility.

Leverage Initial Price and Value: Often, this involves an initial price point that is aggressively competitive to trigger the platform’s “value” algorithms and attract the first wave of price-sensitive customers. The goal isn’t profit here; it’s social proof.

The Goal of Phase 1: Generate volume. Generate sales. Generate reviews. This data and activity signal to the platform that your product is desirable, which in turn feeds you more traffic, creating a virtuous cycle. You are building a business based on a functional benefit.

Phase 2: Pivot to Building the Emotional Moat (The “Brand” Phase)

Once you have a steady stream of customers and positive reviews, you have a foundation. Now, you can begin the work of making those customers loyal and less price-sensitive.

Activate Your Customer Base: You now have a list of people who have had a positive experience with your product. You engage them. You move them from the transactional platform (e.g., Taobao) to a more private and loyal community (e.g., a WeChat group).

Layer on the Story: Now you tell them why your fast-charging cable is better. “It’s made with sustainably sourced materials.” “It was designed by ex-Apple engineers who left to pursue their passion.” “It’s the official cable of a popular esports team.” The functional benefit (fast charging) is now wrapped in an emotional one (sustainability, innovation, community).

Expand the Content Universe: You use Xiaohongshu to show the lifestyle your product enables. You use Douyin to run live streams that are less about a hard sell and more about building a relationship with your founder or community manager. The product becomes a character in a larger story.

This sequential approach is crucial because trying to build an emotional brand from day one is often too expensive and inefficient when you have no social proof or volume to validate your claim.

Example

Perfect Diary (完美日记) is a well-known case study.

Phase 1 (Volume): They exploded by partnering with an immense number of mid- and micro-influencers (KOCs) on Xiaohongshu, focusing on specific, functional attributes like “long-wear lipstick” and “pigmented eyeshadow palettes.” They used data to identify trending colors and released new products at a blistering pace, hacking the content and discovery algorithms to drive massive volume.

Phase 2 (Brand): After achieving scale, they opened immersive, Instagram-friendly offline stores, collaborated with high-profile entities like the Metropolitan Museum of Art, launched and acquired higher-end sub-brands to build a more sophisticated brand identity and foster loyalty.

One of Perfect Diary’s pivotal acquisitions is a brand called Little Ondine – which was a Searchlight client at the time. We helped them rationalize their offline retail strategy by focusing more on visibility than sales, refocused the brand on a more affluent and receptive target audience and guided their ecommerce execution to drive better response rates and volume. We also supported them with guerilla marketing – getting them significant visibility in the London Fashion Week and Shanghai Fashion Week for almost no spend. Little Ondine caught the attention of Perfect Diary and the founders and shareholders exited via a sale to Perfect Diary before they went public.

Sunner Chicken (圣农) is another of our clients who has navigated this journey well. From being a B2B supplier of chicken and other processed meats to leading restaurant chains and fast-food brands, they decided to launch a B2C offering in 2021. As a company, at that time they had very little experience and resource in consumer facing businesses. Even their sales team had no idea how to negotiate activations and visibility with offline distribution channels, leading to situations where we’d go on market visits and find their brands hiding in a freezer until a consumer asked sales staff to go find it for them.

Luckily, and surprisingly, online shopping dominates even the food category, at least in the top 20 cities in China, so we were able to get the client to focus on building an online business first. They did that through the first year while we helped to refine their brand positioning, product mix and targeting and once they had enough of a consumer base, they started to focus on brand building advertising (as opposed to just performance advertising) and rapidly achieved the number one position even on crowded ecommerce marketplaces like TMall, Taobao and Douyin which all had over 1,500 brands of frozen chicken competing for a share of the consumers’ freezer space.

Conclusion

The near “Perfect Competition” of China’s ecommerce marketplace makes it a lot harder for brands to win than other markets, where offline still dominates, not all brands have equal access to consumers, and consumers do not have access to extensive information about a large number of available brands. In this environment, success involves first building a presence, then leveraging that to build a brand in the long term. Done right, brands can rise above the internecine battlefield of the open market and start to build a moat that drives repeat buying, brand premiums and long term success.

At Searchlight Consulting, we help brands grow and cement their success in the marketplace with clear business and marketing strategies supported by deep insights on the consumer and dynamics of the marketplace. Write to us on enquiries@searchlightchina.com if you’d like to talk to us about your business.

China responded to the US announcement of tariffs by announcing its own counter-tariffs, a move which was met with a threat of even higher tariffs by the US on imports from China. Where that escalation will end, nobody knows, but we thought it might be instructive to look at what key categories of goods are being traded between the two countries in the first place, to try and predict what might happen.

The first thing to note is the difference in scale. US imports from China are considerably greater than their exports to China.

The second, quite interesting thing, is the two common categories – electrical & electronic equipment and machinery, nuclear reactors, boilers. The first could be a mix of both consumer and B2B goods, the second looks far more like essentials for setting up plants, factories and powerplants in either country. It would seem that, given the relatively small amounts of money involved in the US to China direction, China will continue to import whatever cannot be replaced by local / other international sources. Very likely they will identify these essentials and possibly offset any tariffs on their import or subsidize the importing entities in some other way. (They will very likely do this discreetly to continue to foster the impression of imposing counter-tariffs on American imports).

As regards other categories, Chinese importers will almost definitely be looking for other sources where possible – particularly with agricultural commodities. Perhaps aircraft and spacecraft related imports will be more inelastic – although on the aircraft front, if any purchases have been committed, they will probably be renegotiated to account for tariffs.

In the opposite direction, it feels harder to imagine US firms and businesses very quickly finding domestic replacement sources for machinery and industrial essentials. The other categories, to the extent that some of them may be consumer goods, may be somewhat more replaceable, but if plastic or electrical / electronic equipment are being imported for industrial use, those supply chains may not be easy to replace with domestic US sources.

When we move on to the other categories, toys, games & sports requisites stands out a a large category that the US imports from China. We know, of course, that most toys are made in China. When this category gets hit with tariffs, prices will go up, consumers will buy less and overall the volume of trade will drop. Given that this is, in some way, a far more discretionary / non-essential category than let’s say food, it is likely that it will drop disproportionately.

Overall, therefore, there may be a significant impact on some of the more discretionary or non-essential categories, but it appears at this time that the US is importing more of those categories than they’re exporting. China, on the other hand, seems to be importing more industrial goods and agricultural commodities, where demand is driven by industrial necessity and it will take time to find alternative supply sources. It does seem likely, therefore, that overall, US imports from China may drop somewhat faster than their exports to China, at least in the 12-18 months of tariffs. Which, for what it’s worth, will somewhat address the trade deficit that was cited as the main motivation for the US tariffs.

However, it is unlikely that the balance will shift so far as to significantly reduce the trade deficit and as time goes by, China will find other places from which to import some of these items – so in a timeframe beyond 18 months, it is likely that US exports to China will also drop further, leading to a trade deficit similar to, or perhaps even worse than, what it is today.

There are, of course, many more categories in which goods are traded and even the very broad category definitions for which we’ve found data are capable of being broken down in much greater detail. For companies contemplating their future, it would be good to study a specific category in greater detail to try and understand what might happen.

Last week, we released an overview of the expected effects of the U.S tariffs on imports in our newsletter – if you haven’t read that yet, you can download it here.

In case you haven’t yet downloaded and read the previous article on the subject of the tariffs, we need to reiterate one very important point from it.

Prices to consumers will go up and demand will go down across most categories in the US

In brief, we outlined in our newsletter that with a price elasticity ratio of 4 and a 0.25 ratio of impact of tariffs on consumer prices (both these numbers estimated by the USTR and shown in the formula for calculating tariffs), the price that consumers pay for a whole array of goods will go up significantly. That will drive a contraction in demand and a significant drop in revenue from the US market for any company doing business there. If you want to read the details of how we arrived at our conclusion, download the newsletter at the link we’d provided above.

Moving on to the topic for this post:

In this post, we wanted to quickly examine what US based companies with significant overseas manufacturing can do to try and retain their market in the US. As we explained in the overview, moving production facilities to the US is not going to be possible in the short or even medium-term.

In order to explore what options US based brands have, we looked at two very different examples.

Nike has significant manufacturing overseas – 95% of shoes and nearly 60% of apparel being made in Asia. However, their are also more diversified in terms of revenue with just over half their sales happening outside the US.

By contrast, General Motors is heavily dependent on the US market for revenue but still has significant imports of parts (49%) and even for finished cars, with one report showing 750,000 cars being imported from Mexico out of the 2.7 million cars GM sold in the US in 2024.

In our newsletter we’d suggested that companies should focus on international expansion since a contraction in consumer demand in the US is inevitable. You can see how this makes sense for Nike, who are already getting 52% of their revenue outside the US. However, it’s going to be a lot harder for GM who get more than 80% of their automobile sales revenue in the US.

In Nike’s case, their best options would be to explore further supply chain efficiencies which can mitigate the effects of tariffs and help them retain as much of their US revenue as possible, while continuing to grow their international revenue and reducing their dependence on the US consumer.

In GM’s case, they’re caught between a rock and a hard place. They clearly are not able to build significant revenue outside the US but are already dependent on the efficiencies that come from manufacturing parts overseas. Perhaps the fact that they’re still assembling a significant proportion of cars in the US, combined with a demonstrated intent to reduce their imports will help them negotiate some concessions on the tariffs they pay for the parts they import. They also have some time before the tariffs on auto parts are imposed, which may allow them to stockpile and focus on assembly entirely within the US for the domestic market.

GM has not been as successful in international markets, as the chart below shows. Trying to suddenly change that and win share in other markets is definitely a hard ask, so their only option is to try and salvage as much of their US business as possible – which means they have to try and do everything they can to minimize the impact of tariffs on consumer prices in the US market. Even with that, the overall rise in consumer prices across the board will definitely cause a contraction of demand for cars and pose a sales challenge for GM and indeed, all the auto majors in the US.

If you run a business that is looking to diversify revenue by growing in China, maybe we can help. We are specialists in helping brands succeed and grow in China and we believe it will continue to be a significant market for the foreseeable future, with a large consumer base and steady economic growth and recovery over the last 15 months. Write to us at enquiries@searchlightchina.com if you’d like to talk further.

Consumer sentiment in China has been somewhat pessimistic over the back half of 2023 and the first half 2024. One category that reflects the propensity of consumers to spend their disposable income is travel and we looked at some recent travel data from over the October holidays to see what it might tell us in this regard.

While domestic travel has recovered to above 2019 levels, outbound travel has some way to go

Different sources estimate that 2024 outbound travel will be between 70 – 80% of 2019 levels. Fastdata estimates around 70% while China Trading Desk estimates closer to 80%. Overall, there is still some way to go for outbound travel to resume, as the table below shows.

Overall, it seems Chinese consumers are as willing as ever to spend money on travel, but the shift towards more domestic travel that happened during COVID is here to stay. Countries that have made visa-free entry possible for Chinese citizens have benefited – particularly Thailand and Singapore, and in 2024 we should see about 70-80% of the numbers we saw in 2019. A full recovery to pre-COVID numbers may take up to 2025. All good and positive signs, however, and a sign that consumer confidence is returning.

Often, taking the time to understand the core problem can lead to a very different solution – sometimes one that doesn’t need a consulting solution at all, or sometimes one that needs new / different skills. Being honest about the real problem and helping a client even if it curtails a revenue opportunity is a core value for us

When your only tool is a hammer, every problem looks like a nail

Every so often I read a post by an advertising person extolling the value of spending money on advertising. Or one by an agency creative director talking about the value of creativity. AI aficionados will talk about how AI can solve every problem. Search specialists think the answer lies in optimizing SEO and SEM…

I’ve never seen an adman advise a client to pull back their advertising and do something else with the money that will have a better impact on the business. Or a creative director suggest that perhaps using influencers or search is a better solution than creating ads. Or a search specialist saying that TV (by which term I also include online video – I’m not that much of a dinosaur!) might work better in a particular case than SEM.

The world seems to be full of specialists who each think his/her special skill is the only / best / optimal solution to a client’s business problems.

We tend to approach each new client with a very open mind. The focus of our first few meetings is trying to figure out what they really need to solve. Sometimes, what a client asks you to solve isn’t the core problem that needs solving, which can lead to some interesting situations like the one below:

New user acquisition or heavy user retention? Or deeper organization / process problems?

One of our first clients was an online flower subscription service. People sign up for a year’s worth of weekly flower deliveries although there were also other one-off bouquets and arrangements you could buy for yourself or as a gift. The client approached us with a brief for helping them understand what their brand should stand for, how they should go about advertising to potential new users and grow their user base rapidly.

Despite their eagerness to focus on brand architecture and connections planning, we suggested that there was value in taking some time to look at their data and understanding their existing consumers before venturing out to look at potential new users. In the process of doing so, we realized that, for an internet platform that had tremendous data about each transaction and user, they had zero visibility on that data through the organization. Marketing decisions were being made on feel, nobody was keeping track of subscribers and the data was in a thoroughly unusable form with the IT department.

When we finally finished helping IT organize the data properly and analyzed it we found that the platform had peaked in user numbers about 3 years prior and since then, had been losing users steadily. Most worrying was the fact that they were losing about 18% of the heaviest users every year, each of whom spent an average of 2500 RMB / year, while new users typically spent less than 200 RMB / year.

When we started to explore the reasons why, we discovered an utter lack of focus on customer retention. The platforms helpline had a woefully inadequate set of responses to customer complaints, there was no tracking of when a subscription ended and therefore no reminders or renewal offers sent out and there were no KPIs around customer satisfaction and retention.

Although it meant an early end to our project, we recommended to the client that they focus on fixing these areas and blocking the leak of existing customers before focusing on any initiatives to attract new ones. We also had recommendations on restructuring the marketing team for a “one-customer” view and better internal systems and processes for making data-based decisions.

Now, think about it. Have you identified and addressed (or are you in the process of addressing) a core problem? Or are you doing something without being clear what the real problem is?

At Searchlight we help clients identify and address the core problems holding them back from success. We work on assignments ranging from market understanding, brand architecture, organization structure, sales training and other core areas of business strategy.

Reach out to us at enquiries@searchlightchina.com for more.

Drawing from a huge database (260 million MAU, 300 million daily searches) we examine what consumers are searching, reading and posting every month.

In partnership with XiahoHongshu we bring you a monthly newsletter packed with insights.

XiaoHongShu is where consumers go to see what their peers are saying about life, the universe and everything – including specific categories and brands. With 260 million monthly active users, over 300 million daily searches and over 90% of it’s content being user-generated, Xiaohongshu is the most authentic source of social listening for China.

This content will not be on our website. Sign up below to receive our newsletter in your inbox.

For a long time now, brands and media in China have been obsessed with the post ’90’s and post ’00’s generation. Is it time to start looking at the other end of the age spectrum for opportunities?

For a while now, we’ve all been reading about China’s slowing birth rate and the stabilization and eventual de-growth of its population. Sometime in the last few weeks, a milestone of sorts was reached when India’s population was estimated to overtake that of China. However, what hasn’t received a lot of exposure is the fact that, due to the many decades of a single-child policy in China, there has been a steady shift in the age-profile of the population and falling birthrates will exacerbate this shift. National Bureau of Statistics data shows the elderly population over 65 years old has been increasing by an average of 2.76% annually from 2000 to 2019. This steady increase against a backdrop of a stagnant / decreasing population will take the percentage of elderly people in China to 35% by 2050.

The aging population is gradually becoming more prosperous, making this an attractive market to focus on. National Statistics Bureau data shows that the number of elderly people with incomes of over ¥100,000 ($15,200) per year has tripled from 19 million in 2003 to 60 million in 2018. This group accounts for 43.9% of elderly consumers, and it is expected to grow at an annual rate of around 8% in the coming years. In addition, the per capita disposable income of the elderly population has increased steadily over the past few years, and it is currently standing at ¥28,341 ($4,313) in 2020. While those numbers lag those of the rest of the population, they are steadily rising, and unlike younger consumers, the elderly have less demands on their income (children’s education, housing, daily transport and so forth).

Future Opportunities and Threats

Today’s middle-aged working population will be in the elderly age-group in the next decade. Given what we’re seeing of the current 65+ population, here are some predictions on what the current middle-aged (45-54 age group) will be focusing on over the next decade:

Greater demand for Investment Products and Pension Funds

Looking at sources of income for current 65+ seniors it is apparent that future income after retirement will be a source of concern both for current and future seniors. China pension funds as a percentage of GDP are not growing in pace with the changing population profile.

There will be increasing demand for financial services and investment products from this age group as they hasten to create an ongoing source of income that reduces their dependence on their children.

2. Real Estate Oversupply

One characteristic of families today, as a result of the one-child policy that was in place for several decades, is the 6:1 ratio of parents/grandparents to each child/young adult. While that policy has now been relaxed, it leaves a situation where every young person has typically 3 pieces (at least) of residential property to inherit over time (home ownership in China is estimated at nearly 90%). One area of investment that is likely to see less interest (pun intended) in years to come is real estate.

3. Healthcare

As one of the previous charts showed, medical and health related expenses are already 22% of the senior group. Additionally, China’s health expenditure has shown a steady growth since 2001 and apart from very recent times, average household expenditure on health has also grown steadily.

4. Elder-care and elder-friendly services

While there isn’t enough data yet to estimate market-size or spending in this area, the last few years have seen the beginnings of new services focused on the elderly, many of which recognize their lower level of comfort with technology.

Opportunities in the gray market

As China’s population ages, the nature of market opportunities that arise will be different than what we’ve seen in the last 20-25 years, which were focused more on the post ’90’s and post ’00’s. The 55+ age group has not been a focus for most companies in the past, but will become increasingly important over the next 10-30 years. Apart from products and services specifically aimed at this group, redesigning or rethinking broader based products with the specific needs of an older group in mind represent a growing opportunity for the future.

At Searchlight, we begin every project with a thorough market diagnosis to understand what has happened before and where the opportunities of the future will come from. This is a vital step in helping companies thinking about their business and marketing strategy.

As China opens up once again, many global businesses that had postponed or toned down their activities and engagement with this market will start thinking about the future. Here are three thingsthat have changed over the last 3 years

Within the space of a week in December, China relaxed all the COVID restrictions that were in place.

We’re now seeing “business as usual” after almost 3 years of various kinds of abnormality. Many international businesses which stopped focusing on China for the past few years will now put it back on the agenda for both management attention and potential investments and market entry or re-entry.

What are some of the things to be aware of as you (re)engage here?

1. Changes in the marketing and sales ecosystem

China’s unique marketing and sales ecosystem has become even more different over the course of the pandemic. Ecommerce has become more dominant than ever since retail shopping was not an option during the early days of the pandemic and the lockdowns during 2022. Social commerce has become a big part of the ecommerce ecosystem – starting to challenge conventional ecommerce for total volume. A relatively new development that is becoming mainstream is “live” commerce – sales generated during livestreaming events by brands and influencers. All of this makes planning a sales, distribution and trade visibility strategy much harder for brands that have not been operating in this environment.

2. Accessing the consumer can be very easy – or difficult – depending on how you do it

Consumers in China have had a very different discovery process since the early days of the 21st century, since conventional “Brand” marketing here had a relatively short history after the opening up of the market in the ’90s. Ever since the early days of e-commerce here, where small companies could set up a store on Tmall or consumers could sell using WeChat, there has always been a “smart” way of getting to consumers. That trend has continued to accelerate as new forms of social sharing media emerge. In a category as prosaic as packaged meat, for instance, there are brands who use Douyin (Tiktok) very powerfully to drive significant volume, but those same brands in conventional e-commerce or even offline retail may not be anywhere near as dominant.

3. Chinese consumers are re-evaluating their lives and relationship with the rest of the world and brands will play a part in that

We have seen changes in consumer priorities from their online searches in Chinese social media as well as qualitative research. Consumers are re-evaluating their lives, the balance of work and leisure, what they do with their leisure and so on. There is a sense of searching for “escapes” from daily life more frequently, whether real escapes through the form of travel or virtual ones. The interest in foreign travel and culture has also revived and there is a sense that consumers will seek out experiences and brands that give them the satisfaction of living their lives more fully than ever before.

(We had covered some of the trends we anticipate in 2023 in our 2023 Outlook report which you can get here if you haven’t yet seen it.)

If you’re contemplating a market-entry or re-entry in China in 2023 and need some advice on how to go about it, reach out to us at enquiries@searchlightchina.com to set up a callor a meeting